The Case For Physical Gold part II

The annual world demand for gold in 2010 was just shy of 4,000 tonnes (mind you there are 35,273.9619 ounces in a tonne). Total world demand for gold is up 9-10% year over year (YoY), the investment dynamics point to a shift from electronic exposure to physical bullion and the value of the gold demand in dollars increased 38%. A YoY decrease of 45% for OTC and stockflows (like GLD) and an increase in physical bar investment of 56% shows that investors are fleeing the derivatives and getting physical. Jewelry demand is actually up even higher YoY at 69%, according to the WGC.

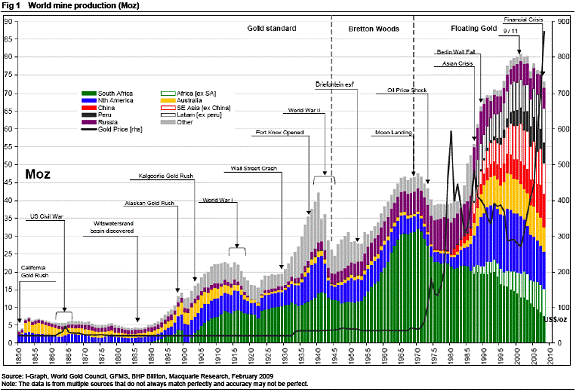

The one force within this movement, that most concerns and interests me, is future supply. European and IMF gold sales have effectively "dried up." Accordingly many central banks have in fact become buyers and the emerging markets are making the most impact. We are receiving less recycled gold from the world and as production ramps up investment demand is there to purchase it and the next 100 tonnes not yet refined. As the currency crisis unfolds investment demand for physical gold will only increase, most likely at levels above production and recycling leaving the option of price discovery freeing up gold at much higher prices as the most likely scenario. Targets of $1610 per ounce for 2011 and $1850 for 2012 are conservative and a great deal of the price action will depend on the Federal Reserve's potential plans for more easing.

Gold imports in China rose 500% from 2009 - 2010 to over 200 tonnes. China also mined over 340 tonnes of gold in 2010. In January and February of this year China had already imported 200 tonnes of gold. This should come as no surprise and we should realize they are just getting started with their gold buying program. China one of the lowest percentages of gold relative to the nation's foreign reserves, they must continue to import gold if they are to achieve stability and or any sort of dominance in the new monetary system that is yet to be upon us. China does not currently allow gold to be legally exported from their soil. The Chinese government has consolidated the gold mining industry this decade and the number of gold producers fell from 1200 to 700 in this time period. China relies on a handful of producers for nearly half or their production supply.

India's gold demand increased 66% from 2009-2010 to 963 tonnes. India's demand for gold currently rivals China and the USA combined. India's citizens are known for saving in gold and silver and giving large amounts of gold during the wedding season which begins in February. As a percentage of gross household savings Indians are saving much more gold.

I simply like to think of those two markets (China and India) as nearly 40% of the world's population. If you can find trend there, it will likely affect the whole world.

Gold will not only retain it purchasing power in real terms, it will gain purchasing power as many investors, nations and common men attempt to flee from overexposure to fiat currencies into hard assets known to shine in volatile times where nominal terms can be so misleading for only so long.

Comments

Post a Comment